Introduction:

More Debt than Money:

The impossible contract.

The Politicians Guide to Money System Collapse

by

Andrew Chalkley

2016

Introduction and Summary

This summary is close to finished. Please send me any needed adjustments before I publish it.

Letter to All

2016-04-01

Dear reader

I assume you want the formula to fix your financial system. To create a solution, it is necessary to understand the way money works for society, for both money and humans are imperfect and the solution, itself, will be imperfect. So a solution is a combination of imperfect components. This is a problem for me as I am a bit of a perfectionist. Money is imperfect because it not able to act as a store of value at the same time as enabling transactions. Money was invented to facilitate transactions and so it needs to act as a temporary store of purchasing power between transactions, but it does not need to hold value any longer than the next transaction. I take you back to a village of old not long after we came out of our hunter-gather stage. Instead of swapping eggs for carrots, we swapped eggs for a universal token as a mode of payment, then walked across town and swapped the tokens for carrots. Humans soon established typical mutual exchange values which we call 'price' and so items have a value measured in tokens. Note that, because every item has a value or 'price', accounts can be created in the common unit of account. This method of mutual exchange is a far superior method of trading that overcomes the inefficiencies of the barter system. Money enables efficient transactions, enables us to set 'values' in the marketplace and, to do so, acts as a temporary store of value. The process works well until someone holds onto the tokens for too long, to use them as a store of value for future use. This hoarding inhibits the exchange of eggs for carrots and so we have the first imperfection of money:

Hoarding inhibits transactions.

The tokens only need to maintain value for as long as a typical exchange occurs. It turns put that the average time taken to the next transaction is critical to the operation of money.

Humans are also imperfect as they tend to maximize for their own benefit, which is tolerable when conducting transactions but not when holding influence over a money system. The inventive nature of humans will cause the tokens to be used for other perceived benefits including hoarding for a 'rainy day' or using tokens to make more tokens or commandeering the supply of tokens or monopolizing the stock of existing tokens or lending tokens. It also includes creating virtual tokens which are traded in a parallel system to the original physical tokens, forming an alternative payment system by transferring virtual tokens. Such is the inventiveness of the human. Another innovation is the practice of: 'lending of tokens and expecting a greater number of tokens in return'. Throughout history, this has consistently been called usury and the practice regularly denounced and often banned because it becomes impossible to pay more tokens than exist.

Usury is the practice of lending tokens and expecting a greater number of tokens in return.

We must never forget that tokens were designed solely for the purpose of exchanging carrots, eggs and apples. Our inventiveness and natural self-interest will cause us to use money in ways that are counter-productive to the original purpose of money which was to enable trade. The whole area of making money from money is an evil, that is not currently recognised as such.

We might imagine the tokens to change hands at least once a day which is three hundred and sixty-five times a year which would be expressed as: Velocity = 365. If we imagine money to change hands once each week, we would have: Velocity = 52. If we perceive money to change hands each month, we would have: Velocity = 12. Modern money commonly changes hands twice a year which is expressed as: Velocity = 2. The reason is that we are not using money for its intended purpose. We are doing any number of things with it rather than its original purpose. Just as in the village, the practice of hoarding tokens inhibits transactions involving eggs and carrots. In our society, the hoarding damages the Real Economy. Possession limits growth. The carrots and eggs section of the economy is called the Real Economy. Even modern day study of money focuses on making money rather than spending money in the Real Economy. If we reduce our expectation that money should move from the apple seller to the egg seller, say, to once a week, then we should expect: velocity = 52. So it follows that possibly only 4% of money is Circulating Money doing the real work of money in the Real Economy at any one time. (2/52=4%) If we reduce the expectation to once a month, then we are requesting money to change hands with a velocity of 12 times a year, which suggests that 17% of money is 'Circulating Money' being used for transactions and 83% is Hoarded Money.

It thus appears that almost all the money is hibernating or used in financial transactions. Humans have run a constant battle against the misuse of money and its use for anything other than trade in the Real Economy. The Real Economy is that part of the economy that is concerned with producing goods and services rather than the part of the economy that is concerned with buying and selling on financial markets. In the modern world, we manipulate the use of money so much and put so much human effort into its manipulation that we watch our Real Economy get destroyed. We import food and watch our industry collapse whilst an army of financial advisers fight to tell us how to make more money from money. If traders have no money with which to trade, there is no economy.

No Perfect Solution

The solution is going to be difficult because there is no perfect solution and the rampant misuse of money has become excessive and normalized. Much of the study of money is directed to ways of misusing money rather than ensuring its appropriate use as a medium of exchange. Even the definitions have been distorted to aid its misuse. So you will need to travel a little journey with me to study the imperfections so you can evaluate a workable solution. It is imperative that I take you on this journey as there is no simple set of rules and many things will improve the economy without being a complete solution. Monetary reform is also very dangerous as you don't want to cause a collapse of the system. Not fixing it is a fairly sure path to collapse, and the collapses tend to be rapid and brutal. If there is a collapse, it will be beyond Mad Max. Food transport to the cities will cease entirely.

Like the punishment of a good father, you will make the system resilient to total collapse. You make the system friendly to those exchanging eggs and carrots in the Real Economy. You will cut the volume of money that is evading the 'eggs, carrots and apples' Real Economy. You will reduce instability. You will collect tax to prevent the oversupply of tokens in a manner that enhances the Real Economy. Surprisingly, there are taxation methods that are fairly painless and actually boost the economy rather than damage the economy, as most current taxes do. You will correct the issue of government debt and a host of other issues on the way. You don't want to bring the whole system down to fix the complaints of the anti-bank people. The anti-bank people are as much a problem as the get-rich-people and their support team of devious bean counters. You cannot entirely get rid of usury but you can get rid of it where it is damaging and dangerous to the banking industry and civilized life. You will change the current 'rampant usury' to a 'controlled usury'. You will need elements of usury to enable easy credit for business entrepreneurship and to allow the banks to make a healthy profit. The bankrupting of occasional citizens is tolerable but the bankrupting of nations is a dead end road for banks that will lead to their demise. We rely on the payment system of the banks to pay bills rapidly, efficiently and over great distances, even between people of different languages. This payment system is utterly fabulous and universally trusted. I can pay my bills from my kitchen table. I use the bank statement to create my business records. I can pay for a new motor for my electric bike from a business in some unpronounceable town in China where they do not even speak my language. The system is highly efficient and almost completely error free. It is a credit to the banking industry to have developed such a sophisticated worldwide payments system. Our modern world is not possible without the payments system and the fees for using it are very cheap. As a database writer, none of my customers match the efficiency and accuracy of the banking industry. During 2014 The USA Automated Clearing House Network handled:

around 18 billion transactions. [10064]

moved approximately $40 000 billion. [10064]

has close to zero errors.

Our problem is not the fantastic payments system, our problem is the horrendous debt that this money system generates. It is a system that consistently generates more debt than there is money available to pay those debts, as I shall shortly to demonstrate. This debt, in itself, is only the small part of the problem, it is the unpayable nature of the debt that is even more troubling. Even the unpayable nature is minor compared to the last problem. As we look at the issues further, it is the instability that is by far the greatest worry. The unpayable debt, the volume of hoarded money and various other destabilizing issues create a situation where a financial crisit will feed its own collapse. You don't want to be on the top of a ladder when you have a heart attack. Don't sleep walk in no mans land.zzz Don't picknic on a cliff edge. The financial instability is like the long slow build-up of snow on a hillside that has become so deep that any moderate trigger could cause a landslide of a size never experienced in the history of mankind. My studies suggest that it is like the recent era of Australian firestorms that have burnt with a ferocity never previously imagined. As we have improved snow landslide management and fire management techniques, we need to do the same with our financial system. The current economic system has the pent-up potential to create a financial Armageddon of a magnitude never seen in the history of mankind. This will be an interesting historical event but it will be unpleasant. People will be fighting with machine guns over a sandwich. It will be a doomsday event that will be in the history books in a thousand years time. And one of the sentences in the history book in a thousand years time will be that the people knew nothing about it ----------- until the day it happened.

Unfortunately, the scenario of a total collapse is entirely possible but also entirely fixable. So we will try and change that sentence in the future history book and the one next to it that says that 'the financial meltdown was so sudden and was of such a magnitude that .......' You can fill in the dots. I give you the chance to alter history. A few months ago, a coloured child was shot in the streets and it caused riots. What will happen if all the ATM's cease to function, all the bank-credit evaporates, no bank transfers can occur and food cannot be transported to the cities? Once the food stores get ransacked, nobody will be brave enough to bring food to the cities for fear of attack. There will be no food. You have no choice but to educate yourself about this as the alternative does not bear thinking about. By the end of the book, you should be able to remove the instabilities and change those sentences in the future history books. I have written this book in a style that even simple people and politicians should understand but it also contains much that is not currently considered by economists.

The money token system has beautifully evolved from the exchange of carrots, eggs and apples in a village. At the same time, the manipulation of the tokens has become extreme. It is hoarded, virtualized, extorted and has led large portions of the population to dedicate their lives to 'making money from money' and accumulating more of it, which is, of course, exactly what you should not be doing with money. Money is solely for the purpose of exchange and hoarding damages its use as such. The village tokens need to be released into society in appropriate volume which might depend on how many eggs, carrots and apples exist. You need to release a few more tokens into society each year as the apple, egg and carrot growers get more efficient. Thus, we release more tokens as the volume of goods and services increases.

A crucial component of a money system is the control over the volume of tokens issued into society.

It is difficult to be sure whether token increase leads to an increase in production of eggs and carrots or an increase in egg and carrot production requires more tokens or both. We release a few more tokens each year as the population grows and we will need extra tokens to make up for those that frustrate the system by hoarding our tokens. Lastly, we need to release a few more to cover anyone lending under usury. The term usury has been softened to the word 'interest'. Usury is a historically much-condemned practice of lending and expecting more tokens in return. When usury occurs, the debts magnify to become unpayable which then requires more tokens to be released to cover the interest. If we don't release more tokens it will be impossible to pay the interest. The USA releases about 5% more tokens each year and China releases about 15%, whilst the UK is all over the place, but is about 7%. Euro Area releases about 8%. To manage your economy you will need to maintain a constant increase in the magnitude of the money supply somewhere in this region. However, this effect can be made by increasing the velocity by decreasing the Hoarded Money. This is difficult because you will find it almost impossible to control the cyclical and inappropriate lending habits of the banks. Driving a car blindfold will be easier than controlling the lending habits of banks.

First, I must lead you through some of the logic of money. We live in exciting times. Debt free societies are possible and have occurred before. National debt is curable. Most of the instability of the system can be removed and much of the environmental damage can be reduced with some smart thinking. Sensible use of money allows the distribution of resources, it energizes the populous to work hard, it shapes the development of the nation and makes us competitive amongst nations and it can be done without debts and destruction.

I wrote this summary of the full book at the request of Dan who I met in Costa Rica one holiday. He appeared to want it for some committee. The summary turned out better than the book and so the summary became the book. It allowed me to build the solution into the structure as I went through. The book developed from a pamphlet I wrote for the Occupy group three years back. I was new to activism. I noticed that activists were good at finding the faults but poor at finding solutions. Whilst writing the pamphlet, two glaring errors poked me in the eye. First was that the official statistics stated that the average debt per person in Australia was $34 000. As an ex-mathematics teacher, I reasoned that it should be zero, as some put money in the bank and some borrow it. The next glaring error was that the tables of money owed to the IMF/World Bank were all negative. All nations are in debt to the IMF / World Bank except four that were zero. This had to be wrong as one half must be in credit and the other half in debt. They are all in debt. So who is the IMF / World Bank? It turns out that the IMF/World Bank are not owned by nations or the United Nations. They are owned by international banks and have a structure similar to any other multinational corporation. They exist to make a profit from nations, not for the communal benefit of nations. Currently, the IMF has accumulated 2814 tonnes of gold [10001] and the Bank for International Settlements 108.0 tonnes. [10001] My further research led to this book.

Money has a few imperfections. It was invented to facilitate trade, to allow more efficient use of resources, to facilitate transactions. It thus has to store the value of the last transaction until it transacts the next transaction. Whatever its value was at the last transaction must be held until the next transaction and so forth. However, it is not always predictable how long it will be held until the next transaction. There must be enough of these value holding tokens to cover for all transactions during a day. So the volume is unpredictable. To maintain value, there should not be too many tokens. Nor should there be a shortage. So management of the tokens is a haphazard guess at best. To ensure that everyone uses the tokens, some level of administrative force is required. So the 'issuing of money' goes hand in hand with control of a society. If someone bucks the system and creates their own money, they get hammered by the authority. If they are a nation, they get flattened, literally. Because the tokens have value, the issuer has an advantage over ordinary citizens in that the issue of fresh tokens gives the issuer an advantage at the first use of the token. This is called seigniorage. If the issuer is constantly releasing (spending) new tokens, then they need to reduce the volume of tokens to prevent an oversupply. Because the volume of tokens required is unpredictable and because it is difficult to predict how long people will hold tokens before re-using them, the rate of removal is not precisely predictable. So some flexibility needs to be built into the system, so that tokens are available on demand. This is particularly relevant to business where an increase in workload requires more tokens for a short period of time. If tokens that are surplus to requirement are not removed, excess tokens build up and dilute the pool of tokens in a process called inflation. It is difficult to predict how long people will hold tokens before reusing them. A milkman restocks his milk cart daily. A shop restocks weekly. A shirt shop may restock monthly. A beggar spends within minutes. A wage earner may be broke in one week. So the number of transactions completed by money in one year is not predictable. One might expect it to be twelve times a year. In most countries it is two or less. There is a big problem in society with Hoarded Money. This Hoarded Money, if all spent at once will overwhelm the volume of goods and services and cause massive inflation of even hyperinflation.

The imperfect nature of money is easy to see when you consider the ways we use money:

Money is prone to hoarding by people with more than they can spend. They steal it from the circulation like removing the balls from a pool table, mugs from the tearoom or the coins from the carwash.

It can be lent. People with more than they need, may lend it to those that need money tokens for some reason. If the borrower is required to pay back more than they borrowed, it is possible to have more owing than there is tokens.

Substitutes can be created by writing on a certificate: "I owe the bearer of this certificate one token" and "collect it anytime you want!". Yet the lender may not have the token that that the certificate represents. The token supply has effectively increased by the number of unbacked certificates.

If the volume of substitute tokens is high and they are lent into society at say 10% interest, it is easy to have more debt than money. If there are 100 tokens and 100 certificates, within eight years there will be over 200 tokens owing to the certificate issuers. In thirty years there will be 1744 tokens owing to the certificate issuers, yet there is only 100 tokens and 100 certificates in circulation. Yet the naughty certificate issuers never had the tokens that backed the certificates in the first place. The money system is no longer functioning for the benefit of society. The certificate issuers have bought the land, assets and politicians.

The system is collapse-prone. If trust in the tokens evaporates, the people revert to barter.

If money is hoarded, it can all come out of hiding in one day and flood the system causing loss of confidence.

More Debt than Money

When I explain the logic of money to people, I first demonstrate that it is possible to have More Debt than Money. Initially, people find this difficult to accept. I get some seriously puzzled faces when I demonstrate this mystifying phenomenon. I could not believe it myself when I first discovered the situation, so I worked on numerous ways to confirm to myself that this was truly the case. I give three examples and then a graphical representation to demonstrate that there can be More Debt than Money.

My first example:

Imagine the time when gold was money. Imagine all the gold in the world. Imagine all the gold in the world is lent out by those that hold the gold. Interest is payable at 10%, in gold. At the end of the year, how is it possible to pay the interest? How can you pay back more gold, than there is gold? The interest has done something very strange, it has created unpayable debt! Money has created unpayable money. The process of expecting more in return than was lent is called Usury.

The next example:

Consider all the money in the world that has been created by the central banks of all the nations of the world and imagine that all the money is lent out at 10%. How can the interest be paid? How can we pay back more money than there is money? The banks want more money than all the money. This Usury is a major feature of our money system. Our modern money system creates More Debt than Money. Our money system creates more debt than can be repaid with the money in circulation. The creditors want more money than all the money that exists.

My third example:

There are ten people in a room that represent the people of our nation. You are one of them. I am a bank and I will lend each of you one hundred money tokens which we shall call dollars. The interest rate is 10%. You may trade with each other, build each other houses, and carry out regular business.

It is now the end of the year and I want my money back and you each owe me $110. If you cannot pay, you can give me your real assets. In days gone by, this would have included enforced servitude or even your wives and daughters taken as concubines.

This, clearly, will not work. So the first thing we learn is that it is possible to have More Debt than Money. More Debt than Money means that the debts are unpayable. If the debts are unpayable, then an Impossible Contract has been created. If this Unpayable Debt is an Impossible Contract, is the debt legal? I don't have an answer to the legality of Impossible Contracts, but they appear to be very common. I call this:

The First Flaw of Economics

It is possible to have More Debt than Money.

Asset Stripping and Default

If an economic system generates More Debt than Money, it is a flawed system. It is characterized by Unpayable Debt and constitutes an Impossible Contract. The debts are uncollectible. The debts are unpayable. Default, foreclosures and asset stripping are inevitable. However, we can live with some usury. Individuals die and their debts die with them or their houses get repossessed. This is uncomfortable but sustainable. Debts to governments, however, are sustainable until the nation is stripped of its assets. From then on, a default is inevitable. A nation cannot be foreclosed or repossessed, and so a default is inevitable. Various interesting terms are used such as: 'bailout' and 'haircut'.

| 'bailout' | = | Create and advance more virtual credit to the nation so that the nation can pay the interest on the previous loan. This avoids killing the horse that allows the banks to scalp the public. |

| 'haircut' | = | The debt or interest is reduced to a payable level. The bank only lent credit that it created out of thin air. The money did not originate from a central bank. |

There are some obvious solutions but nobody seems bright enough to use them:

The government mints a coin with one trillion dollars stamped on it. It uses this Trillion Dollar Coin to pay off its debt to the banks.

The government creates a Public Bank. This bank is owned by the government. It lends money to the government when prudent. The government thus owes money to a government bank which makes the debt irrelevant.

The government creates a digital version of cash. This would be real or virtual currency notes where the serial number, a digital picture and an ownership history of the note are stored on smart phones, smart cards and anonymous cards like metro cards. The digital data is passed instead of a paper note with its serial number. This is different to the bank system where you have a balance of credit for money that never existed. In this system, you own the notes as you would have title to the notes and it would be recorded in the same manner that land titles, car registration and domain name titles are recorded. Thus, there is no reliance on a single computer system. As with land titles, vehicle registration and domain names, ownership details get updated when appropriate, rather like using a credit card on an aeroplane or ship. The updates can be done at the next convenient time.

The fourth example of unpayable debt is an examination of the figures for Australia:

You now study The Reserve Bank of Australia. The RBA to date has created a total of $67 billion currency in the form of cash folding notes. This is the total of the money created by the Reserve Bank up to 2015. It has created no more than this $67 billion. All figures in this book are in billions and mildly rounded, so remember $67 billion. The total Money Supply for Australia, (officially called M3), is $1760 billion, which is misleadingly called 'Deposits'. Clearly, the $1760 billion did not come from the Reserve Bank nor was it generated by the Reserve Bank. More on this in a while. However, we have noticed that there is a lot more money in circulation than the money created by the Reserve Bank. The next discovery is even more startling. The total debt in Australia owed to lenders is $5400 billion. (as listed by the Australian Debt Clock.). As a society, we owe more Australian money to the Australian banks than there is Australian money. In round figures: The total debt in Australia owed in Australian dollars exceeds the total money in Australia by a factor of three. Do not think that this is an Australian peculiarity. Almost all countries have the same scary 'debt to money' situation.

Back To Our Village

In our village scenario, this situation arises when only, say, one tenth of exchanges for carrots and eggs occur using original tokens. Most transactions now occur using borrowed tokens. It occurs like this: There are insufficient tokens to make for egg and carrot trade efficient, but a generous person who claims to have 'excess' tokens, offers to loan you tokens at 10% interest per annum. The token-lender says that he will keep the tokens in his vault and that when you wish to pay someone he will transfer the tokens to the other person. The token-lender says he will give you real tokens if you really need them at any time. You now trade eggs and carrots for these virtual-tokens. Soon, almost all trade is done using virtual-tokens from the token-lender. Soon your village society has 100 real tokens and 1000 virtual-tokens. The token-lender demands interest on the 1000 virtual-tokens each year which amounts to 100 tokens each year payable in tokens or virtual-tokens. Clever you, will spot the impossibility of paying the 100 tokens because that would leave your village with no real tokens. What occurs is that the debts build up or the token-lender creates and lends more virtual-tokens. Either way, the debt increases as follows: 1000, 1100, 1210, 1331, 1464, 1610, 1771, 1948, 2143, 2357, 2593 [10 years], 2853, 3138, 3452, 3797, 4177, 4594, 5054, 5559, 6115, 6727 [20 years],7400 ,8140 ,8954 ,9849 ,10834 ,11918 ,13109 ,14420 ,15863 ,17449 [30 years]. Yet you have only 100 real tokens. Usury is a mathematically impossible menace. The village collectively owes 17449 tokens to the token-lender even though the token-lender may not even have had any genuine tokens to start with. Anyone could set up this lending system because the lenders are not lending out real tokens. They are lending virtual tokens. They are lending tokens that do not exist. However, you would be hard put to run your village with only the real tokens because your village chief has not issued enough tokens and because the virtual-tokens are easier to use and because business needs money or credit before it can operate. The village chief was not up to standard on each of these three.

The Village Chief

As village chief, your task is to ensure sufficient real tokens are released into your village so that resort to borrowed virtual-tokens is less necessary. In reality, the token-lender never had the tokens that were lent out, but the virtual-tokens did enable trade whilst there was a shortage of real tokens. The token-lender had another benefit to society. The token lender would extend credit to business to allow expansion of business and to cope with the fluctuation in the money needs of business. The village chief spent money into society which created an inflexible money supply. His input did not give on-demand supply of money in line with the needs of business. Business needs money when it needs it, not to buy fancy cars, but to purchase stock for the Christmas rush. Businesses cannot expand if they cannot obtain capital. The village chief was not aware of this and only spent money into society on a random basis. This was good for general employment, but hopeless for expanding business. If the chief were to run small local banks that lent to farmers and business to carry them through tough times or to buy better equipment the businesses would be less likely to scurry to the token-lenders. The money supply expanded in harmony with the needs of society whilst the village chief had issued insufficient real tokens. The borrowed virtual-tokens had accumulated interest that was impossible to pay. So the token-lender finished up owning almost all the real assets and land in the village. The token-lender generously funded your re-election because you were inept at issuing real tokens. The token-lender then dictated policy to the democratically elected chief. This was why all major religious texts forthrightly condemned the practice of usury as it deprives the village people of their real assets. The religions texts forgot about the needs of business. Business needs money tokens before it can create an income. One of your problems is that the virtual-tokens are readily available and easier to use. As village chief you started to use virtual tokens from the token-lender because they were easier to use, which led to your second problem, the village administration became in debt to the token-lenders. And yet another problem was that you as village chief lost control over the number of tokens in society. The village chief was no longer spending tokens into society, the token-lender was lending virtual tokens into society. If the token-lender lent more tokens than he collected in repayments the token supply increased and if the token-lender backed off on token lending, the volume of tokens in society decreased. The decrease caused business collapse and hunger which was blamed on the chief with claims that you were incompetent at economic management. Don't entirely blame the token-lender. The token-lender expanded the money supply in line with the needs of business. Unfortunately, the token-lender got carried away and got citizens and governments into debt. As an individual citizens are a little like businesses. You need to look after your future. You need to educate yourself in real-world situations both in schools and as many jobs and real work situations as possible. You need to look after your reputation. Like a business, you may need to borrow to buy the appropriate clothes and car to get the job. Government only arranges the job and pays in arrears, whereas a bank will give you money before you earn the money. We don't want to destroy the banks, we want them to behave. That will take understanding and regulation and some adjustments to government money procedures.

Richard Henry Dana 1867

After the discovery of America, capital was in demand, and men were ready to pay interest on it. Then the theologians were obliged to review their teachings. If it had come to this, that money must be had, and men would pay interest on it, ecclesiastical ethics must be revised.

If business people do not have money to start or expand a business, they are keen to borrow money or credit or anything that looks or acts like money. Bank credit fulfills this role. The bank-credit never came from a government bank but is has the same effect, it enables transactions. Even though it does not exist, it enables trade and is available on demand. The more business needs, the more the banks create. It is ideal, until it collapses, which usually coincides with excessive greed in the finance sector. Nowadays, the banking sector is more interested in making money from money rather than assisting business to grow. On occasions, they will withdraw funding and take over the assets of the businesses they were previously supporting.

The Value of Transactions in Cash

Although the volume of cash currency in nations is generally less that 5%, the value of trade carried out with cash is even less. According to the US National Automated Clearing House Association, in 1995, $533 000 billion was transferred by wire, $11 000 billion by Automated Clearing House and $800 billion by credit card, $73 000 billion by check and $2 200 billion in cash transactions. [10063] This gives a total of $620 000 billion of which a mere $2 200 billion was in cash transactions which is 0.35% of the total transaction value. However, I am not confident that they have covered all cash transactions. So we have: Less than 5% of money is in the form of government created cash currency, and less than 1% of the total value of transactions is conducted using cash currency.

US Money Supply and Debt Figures

| Currency created by the Federal Reserve | : | $1 250 billion | [10002] |

| Total Money Supply (M2 not M3) | : | $12 010 billion | [10002] |

| Total Debt | : | $43 290 billion | |

[Dec 2014 in round figures. US National Debt $17 820 billion (Federal Reserve), St Louis plus US Private Debt $25 470 billion (Bank for International Settlements)]

(Note: M3 is not published in the USA, which distorts the result somewhat.)

(Note: I use round figures throughout the book as we are dealing with concepts, not high finance.)

(Note: I avoid using trillions and quadrillions. All figures are in billions.)

In the village terms these USA figures are equivalent to the bizarre scenario of:

| Real tokens | = | 100 |

| Virtual Tokens | = | 860 |

| Tokens owed to the token-lenders | = | 3450 |

[This is the same ratio as USA.]

As chief of the village, you have inherited a money system where there are 100 original tokens, 860 virtual-tokens that do not exist and 3450 tokens are owed to the token lenders. Your task is to get out of that situation.

And some graphs that I have created to scare you:

In my graphs, the orange is the total cash currency created by the central bank. The green line is the money supply of the nation. The green is credit created by banks. Notice the almost insignificance of the orange part. In your village, the orange represents real tokens, the green represents the virtual-tokens and the red is tokens owing to the token-lenders. Your village is now operating on credit rather than tokens. For each genuine token in circulation, there is now thirty borrowed virtual-tokens and eighty tokens owed to the token lenders.

Some Scary Graphs

Australia has significantly more debt than the total money in the nation.

The ratio of Debt to Money is about 3.0 [$5400 billion divided by $1760 billion]

Amongst the total collective of all debtors and mortgage holders in Australia, only about one-third of their debts can be repaid.

Australian banks list these debts as assets. Only one-third of these debts are collectible.

Only about ~ 3.5% of the money in Australia was created by the Reserve Bank of Australia. [$1760 billion divided by $67 billion] We are running the nation on credit.

Impossible Debt

Interest on anything of fixed supply creates an impossibility. Let us blame arithmetic for creating an impossible situation where there is more money owing than there is money. It is one of the imperfections of money with which you will have to deal. The very mathematics of lending money creates a situation where the money owed to the lender exceeds the total amount of money in existence. When money is lent, the debt is magnified with interest but the volume of money remains the same. Over a whole society, this becomes problematic, because total debt exceeds the volume of money. Just considering Australia and Australian dollars alone, there are nearly three times as many Australian Dollars owing to Australian Banks than the total volume of Australian Dollars in existence. Very few countries escape this payment impossibility. Europe has a debt to money ratio of about two point six. Greece is about three and the USA is about three and a half.

You may see at least two reasons why the debt cannot be repaid. The easy answer is that there is more debt than there is money. The green is smaller than the red. The green could only pay off about one-third of the red. I may need to prod your brain for you to see the second reason: The green part is the essential circulating medium. It is the money that flows from person to person as transactions occur when goods and services move between persons. Without the green, the transactions cease and we have no economy. Thus, the green cannot be used to pay off the red because the green is the essential circulating medium. No money, no food, no farm produce. Even a failure to constantly increase in the green causes a recession as in the graph of Spain:

A fall in the volume of green causes a dreadful recession called a depression as in the graph of the Great Recession:

It is thus impossible to use the green to pay off the red. So the lenders need to create more loans to keep the system running. More loans are issued to ensure that interest on previous loans can be paid. If more loans are not forthcoming, the interest from previous loans cannot be paid. To keep the present money system functioning, total debt has to grow constantly and the debt can never be repaid and interest is paid with freshly created loans. We are loading the future generations up with unpayable debt. If by chance the banks refuse to grant credit, the nation is plunged into financial paralysis for lack of circulating medium. Whole industries collapse and individuals are bankrupted and the whole charade typically gets blamed on government incompetence. Sometimes even the banks collapse. All the bank needs to do to create paralysis is to collect loan repayments whilst resisting the issue of new loans. This causes the green in the above graphs to shrink as in the case of Greece (and Spain to a lesser extent). The whole of the modern money supply is issued by banks as a loan and the banks have total control over the size of the money supply and thus over the health of the economy. The talking heads will have you believe problems are the fault of the government and the lazy people. Hopefully, you are not that easily fooled. If you would like one of these graphs for your country, let me know, I most likely can get the data and compile the graph for you. Sometimes I have problems obtaining 'Currency' and 'Private Debt' figures and sometimes the data is obfuscated. It can take significant time to data-crunch as the dates can be in an inappropriate format.

To constantly increase the volume of 'green' Bank Credit, there is a need to create new loans. New loans require new items on which to hang debt. The land is already divided up and debts hung on the land titles. Cars hold loans. Education is now on the list. More than 95% of all money in circulation is a loan. We are living on credit. Less than five percent of the money we use came from a central bank. The €30 billion that the IMF lent to Greece did not come from the ECB. The person who has this Bank Credit against their name in a bank account is not paying the interest but the person who took out the loan that created the Bank Credit is paying. Let us do some elementary mathematics. Let the interest rate be 10%. For each $1000 of Bank Credit in a bank account, someone else is servicing $3000 in debt. This $3000 accumulates $300 interest per annum. This is expensive money. If the interest rate was 5%, The interest would be $150:

$1000 in circulation costs someone else around $150 per annum in interest.

This can be corrected and there are a few remedies you can apply. One is to significantly increase the orange portion. One such way may be called the 'Trillion Dollar Coin solution'. Your government mints a coin with a face value of one trillion dollars and uses this to pay off the government portion of the debt, commonly called the 'National Debt'. Another is for the government to create a public bank. This bank is owned by the government and interest accrues to the government. The government borrows money from a bank that it owns. Government debt is thus owed to the government. Interest accrues to the government and the debt is somewhat irrelevant. Australia had this system in 1911 and then became the most prosperous nation in the world. Other countries have used public banks with remarkable results. The Brics countries, Brazil, Russia, India, China and South Africa, all make heavy use of public sector banks. Between 2000 and 2010 they had an astonishing GDP increase of 92%. Public Sector Banks compose about 69% of the banks in China and has made massive progress transforming itself into one of the world's major economies. It has released enormous entrepreneurial energy that created trade and income growth on a scale the world has never seen before. It does not let corporations mess with the government. In the following graph, the purple region is debt owed by the government to the government:

Being a bank, it is in the payment loop with the other banks of the nation where Bank Credit is transferred from account to account to effect payment between citizens. It is difficult for the treasury to do this as it is not a bank and thus does not operate within the bank transfer system and does not adhere to the principles of double entry bookkeeping when it creates new money. It creates money without associated debt. It does not create Bank Credit which always has attached debt, it creates currency which unfortunately has various disadvantages in the modern world. Digital money is the money of choice in our modern world. So I will shortly create a digital money system for your nation that is an extension of the cash currency system.

The Lunacy of National Debt

Here is the next economic oddity. The talking heads constantly tell us that government needs to balance its budget and that governments have clocked up too much debt. Citizens start to believe the argument that taxes must be increased or the government must cut spending to reduce the 'National Debt'. These talking heads engage in endless arguments in a debt blame game that avoids two obvious sensibilities. You can blow their reasoning out of the water with two simple questions:

Who has the authority to create the money of the nation?

Why would a government be in debt for money that it has the authority to create?

There is a common-sense reason, but I'll leave you guessing for a while. You may even grasp the logic before I explain it.

The Second Flaw of Economics

Balanced budgets are a nonsense.

This is a major fallacy in modern economic thinking. It is entirely incorrect to think that the government taxes in order to have money to spend. They are, after all, the entity that is duly authorized to create money.

In times gone by, National Debt did not exist. It was not that the debt was zero, the expression 'National Debt' did not exist. Governments did not borrow money because they did not need to borrow money. Be sensible, Governments are supposed to create money. When operating correctly, governments create money and spend it into society and they tax money back out of circulation to prevent an oversupply of tokens and to create a demand for money. A government need never be in debt for its own money. Let us put that in headlights.

Which reminds me of a beautiful story that I read in a fascinating book by Warren Mosler:

The father of a family gives his children a business card each time they do a good deed or do some work around the house. They occasionally do odd jobs but there is no great keenness to do so. The business cards effectively have no value and have been thrown in a drawer. The father gives an edict that they must give him a number of business cards, weekly, as rent and some business cards for meals. The business cards immediately have value and are much sought after. The young are keen to carry out chores to earn business cards.

The effect of the family taxation was to give business cards a value and to make the inmates productive. Warren Mosler demonstrates the logic behind taxation in your nation. Taxation should occur to prevent an over-supply of money and to create and maintain a demand for money. In this family, business cards are not taxed to obtain revenue. The father can create any amount of business cards at no cost. Taxation and money creation are intended to work hand-in-hand to form a money system. One requires the other. However, the system has gone horribly wrong. Banks create money by lending. They remove money from the money supply by collecting repayments. The magnitude of the money supply depends on bank lending and collection. These are subject to fluctuations that are out of the control of government and only partially controllable by banks.

Do not fall into the trap of thinking that: all the government needs to do is spend money into society. Most businesses need money before they can conduct trade or supply a service. The corner shop needs to buy stock, buy plant and pre-pay rent before the shop earns its first cent. Government money spent into society does not provide this. The trader needs money or credit before business commences. The inventor needs dollars before he makes a dollar. Government is clumsy and inept at providing this service. Local Commercial High Street Banks have been remarkably good at providing credit to businesses. Commercial (High Street) Banks increase the local money supply on an 'as-needs' basis for each and any business that needs trading money and these Commercial (High Street) Banks are experts in evaluating the risks. Herbert Hoover, President of the USA between 1929 and 1933, put it this way:

Let me remind you that credit is the lifeblood of business, the lifeblood of prices and jobs. [10003]

Without access to money or credit businesses cannot get past the 'idea' stage and existing businesses are stifled. In your village scenario, how would a banana trader collect bananas from a distant tribe if he could not access some money to purchase the bananas in sufficient quantity to feed your village? As village chief, you would ensure that he was able to access sufficient money to go on the banana fetching expedition. Governments are poor at doing this. Sometimes family and friends will supply funds, occasionally a government development bank will provide funds, but mostly it is a local commercial bank that provides funds.

Self Interest

People have a tendency to look after their own interests. The operation of a financial system is no different. Thus, the concept that the system should operate as a free market is flawed. The money system must be strongly regulated by others than those that benefit from the system. Self-interest should be completely eliminated from the regulation. In simple words: People maximize situations for their own financial best interest, so most financial transactions will reach a balance. The same argument should not be applied to those in charge of the system. There is a tendency for participants to maximize the situation for their own benefit and so the money system needs to be heavily regulated so that the system does not favour those at the top of the food chain.

These are not new issues. Sir James Steuart from Scotland recognized this when he wrote about economics, including Public Debt and Banking in England, before the French Revolution. This was nearly 250 years ago and about seventy years after the Bank of England had been created by a group of private entrepreneurs as their own cash cow. This powerful book was overshadowed eight years later by a much-feted book by Adam Smith that was somewhat more gentle on the banking profession. James Steuart mentions the 'new' institution of 'National Debt' which occurred when a small syndicate of private business entrepreneurs created the Bank of England. It was a bank but it did not belong to England. Steuart believed that economic development must be purposefully managed by the state. He believed that private self-interest would be counter to the best interests of the nation. The statesman should safeguard the public good and the economy should be regulated to prevent self-interest overriding public good. He believed that allowing the creditor class to regulate the creditor class with its hold on finance was a recipe for disaster. His writing was overshadowed by Adam Smith who advocated that individual self-interest would allow a self-adjusting economy being led by an invisible hand. The book by Adam Smith got heavy promotion and his 'invisible hand' is more like an 'invisible hand' in the till.

James Steuart 1767

Europe was possessed by our ancestors free from taxes; our fathers saw them imposed, and we now see how fast they become mortgaged for our debts.

James Steuart 1767

Let us now suppose what is actually the case in Great Britain, that from the swelling of public debts an enormous fund of personal property is created. This is formed out of the income of the whole nation; and as it has been purchased by those who have lent money to the state, in common language it is included in what we call the monied interest: ....

Smiley face translation into modern wording:

James Steuart 1767

They carried their views to nothing less than obtaining a majority in the house of commons, by the weight of their wealth, and of becoming the absolute rulers of the nation.

James Steuart 1767

By the first step, namely, by refusing credit, it appears passive only in allowing natural causes to destroy both the bank and the nation, as I think has been proved.

James Steuart 1767

but how often do we see ambition putting on the face of public spirit, and animating the resentment of a nation, under colour of providing for her security? Hence wars, from wars expense: recourse is had to credit

James Steuart 1767

This was the case, in the example above cited, when seven millions ready money, borrowed by the late king of France, became a debt of thirty-two millions on the state.

This was not a nice book for the creditor class to have in the public arena. Conveniently, Adam Smith came forward with a book that was promoted, whilst James Stuart was decried as an 'old mercantilist', whatever that means.

This was not a nice book for the creditor class to have in the public arena. Conveniently, Adam Smith came forward with a book that was promoted, whilst James Stuart was decried as an 'old mercantilist', whatever that means.

Just to check that you actually looked at the diagram:

What date did the National Debt start?

What date did the Bank of England open for business?

UK Parliament enacted an income tax that became effective in 1799. This was a new tax.

What is National Debt? National Debt is money owed by the Government. To whom does it owe this money and where did the lenders get the money that the government borrowed?

Now I will test your ability to think logically. You will hear talk about 'paying off government debt':

Why would a government, that has the authority to create the money of the nation, be in debt?

To whom is the government in debt and why?

Who made the money that the government borrowed?

Where do they get the money that is lent to the government?

Under the current national financing arrangements, the way forward involves the nation and its individuals getting deeper and deeper in debt to the private banking system.

The Thirtieth Flaw of Economics

Never forget that national debt is owed in a currency that the government is legally entitled to print.

Unfortunately, we now have a system where the government only makes less than 5% of the money of the nation as cash currency. Banks make in excess of 95% of the money supply. The government no longer uses cash currency to pay its bills. It uses bank accounts containing virtual Bank Credit and thus like ordinary citizens it needs to add credit to its bank accounts before it can use the Bank Credit. It does this by borrowing the Bank Credit and promising to pay it back in the future. The mechanism is to issue IOUs with a promise to pay back the money in the future with interest payments at regular intervals. These IOU's are called Bonds in most countries and called Gilts in the UK and Securities in Australia. Unfortunately, the government loses the ability to control the size of the money supply through money creation and taxation and has to constantly borrow more to keep up the functions of government and pay interest at the same time. The control over the size of the money supply has been removed from government and is becomes dependent on the lending mood of banks. The size of the money supply is solely dependent on the rate at which banks collect loan repayments and the rate at which the banks create new loans. This is a rather bizarre way of controlling the money supply of a nation. Governments have a most strange way of increasing the money supply by getting further into debt and spending the money. It is the act of borrowing that increases the money supply and spending just moves it from government bank accounts into the hands of the citizens. If by chance the citizens are reluctant to take on more mortgages and car loans, the government can borrow and then think of some way to spend it into society. Thus, the apparently idiotic statements about boosting the economy by deficit spending. The only way to keep the system going is to take on more debt. Either the people take on ever more debt or the government does it on their behalf.

What is in a Bank Account

It turns out that the so-called money that we have listed in our bank accounts, is not money as we think of it. It is credit. It is credit on the banks books which you can transfer to others as a means of payment. It is Bank Credit that you can convert to cash currency. It did not come from the central bank. The banks do not have $1760 billion of cash sitting in vaults and $1760 billion of cash does not exist. Only $67 billion of cash exists and most of that is in people's back pockets. Now we sniff out where the money listed in bank accounts came from. The Reserve Bank of Australia has created $67 billion of cash currency. The government does not pay its bills using cash. The government pays for things using bank accounts. Consider what you do if you want money. For little items, you pay with cash or from a bank account. For large items, you will borrow the money. And here is the clue. If you want more money than you have in a bank account, you borrow it. Money is available if you borrow it. So consider the borrowing mechanism. You walk into a bank and ask for one million dollars to buy a house. The bank looks at you and says 'ok'. On the appointed date, the bank transfers one million dollars to the seller by writing one million dollars with a plus sign next to it in the sellers account. It writes one million dollars against a new loan account in your name with a minus sign next to it. One million dollars with a plus sign and one million dollars with a minus sign makes zero.

However, the nation now has one million dollars more money in the nation and one million dollars more debt. No transaction occurred at the central bank. No money moved from a vault. No customer deposits were required. And thus, money creation occurs when banks lend money. This is one of many ways of arriving at this conclusion. I am not a lone voice in the wind. There are many statements about this characteristic of our money system all discussed in future chapters. Here are just a few of many:

Bank of England

Money creation in practice differs from some popular misconceptions - banks do not act simply as intermediaries, lending out deposits that savers place with them, and nor do they 'multiply up' central bank money to create new loans and deposits. ......

money is largely created by commercial banks making loans. ......

money is largely created by commercial banks making loans. ......

Indeed, viewing banks simply as intermediaries ignores the fact that, in reality in the modern economy, commercial banks are the creators of deposit money. This article explains how, rather than banks lending out deposits that are placed with them, the act of lending creates deposits - the reverse of the sequence typically described in textbooks. ......

Commercial banks create money, in the form of bank deposits, by making new loans. When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created. ......

Bank deposits are simply a record of how much the bank itself owes its customers. [10004]

Ralph Hawtrey, Former Secretary of The British Treasury

Banks lend by creating credit. They create the means of payment out of nothing.

Bank of England 2014

Is it difficult to believe that the Central Bank with the blunt instrument of interest rate control can control private corporation lending habits. As inflation continues to flourish, their control appears to be a carefully controlled myth. ...

Creating money in the form of cash notes is illegal and called counterfeiting, however creating money that is equivalent to cash and lending it to people is apparently legal. [10004]

Marriner Eccles, Governor of the Federal Reserve. 1941

If there were no debts in our money system there wouldn't be any money.

Robert Hemphill 1934, Credit Manager of Federal Reserve Bank, Atlanta, Georgia

This is a staggering thought. We are completely dependent on the Commercial Banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the Banks create ample synthetic money we are prosperous; if not, we starve. We are absolutely without a permanent money system. When one gets a complete grasp of the picture, the tragic absurdity of our hopeless position is almost incredible, but there it is. It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon.

Fractional Reserve Banking

Many students of economics were coached to believe a fictional story about 'Fractional Reserve Banking'. This is incorrect and misleading. When a loan is made, no reserve is required. At the moment a loan of one million dollars is made, one million dollars of Bank Credit is created and one million dollars more debt is created. No bank or customer money was required. No transaction or contact with the central bank is required. The mechanics of money creation does not require money from any other source. However, after the new credit is created, there is more money in the nation so all banks will need a little more stock of ready Bank Credit as there is slightly more Bank Credit in society that can be moved. However, this reserve can be borrowed. Fractional Reserve banking is a red herring to mislead you from the actuality of the mechanics of credit creation and cover for the reality that new Bank Credit is created without any backing. Even the Bank of England states this:

Bank of England 2014

Another common misconception is that the central bank determines the quantity of loans and deposits in the economy by controlling the quantity of central bank money - the so-called 'money multiplier' approach. [10004]

Bank Lending and the Great Depression

This characteristic where our money supply relies on the lending habits of lenders is starkly shown in this graph of the Great Depression. When debt repayments exceed creation of new loans the money supply shrinks and there is close to nothing that the government can do. When banks fail to create more loans, the money supply shrinks drastically causing a depression with numerous business failures as the Circulating Money dries up. Notice that the orange component created by the government (cash currency) does not decrease. This problem is not caused by government:

Notice that the Bank Credit portion of the Money Supply decreases whilst the government issued cash currency increases slightly. When the Money Supply fails to increase in line with an increase in population and trade, a recession is felt by the people. When the Money Supply falls, the effect is felt by the people as a depression. A severe recession is a depression where businesses fail and unemployment increases. From the graph, you can see that this is caused by bank lending practices causing a fall in Bank Credit. Try not to be fooled by the media suggesting it is poor government management.

Bank Lending and the Greek Depression

The problems in Greece are similar. Cash issued by the Central Bank of Greece has not decreased. The credit issued by banks has decreased. When banks switch off the supply of credit, a recession or depression occurs. The government has no facility to make banks create fresh Bank Credit. You will have more luck pushing a piece of string. The Greek economy is in a depression because there is a lack of working capital for business. Business cannot obtain funding because the banks will not extend credit. There has been a dramatic fall in Bank Credit similar to that in the Great Depression. This is worsened by the Eurozone's destructive request for Greek austerity. So, under instruction from the IMF, the government is required to cut spending and increase tax rates, both of which magnify the bank created problem.

Debt to Banks

Now I will show you an even bigger problem than the debt in bank accounts. The debts are magnified by interest. The debts magnify whilst the available money remains constant. The result is unpayable debt and the process is called Usury. Perhaps you can understand my diagrams:

Consider the situation in ten years:

This creates an unstable money system. Only $67 of $1760 billion of the Money Supply in Australia comes from the central bank. This is 3.5%, in round figures. Where such a small portion of the Money Supply comes from a government authority and so much depends on the lending habits of banks, the system becomes unstable. Any fluctuation in the volume of loans issued by banks affects the volume of vital circulating medium. This tends to create booms and busts. The busts being the recessions and depressions. The citizens are constantly paying back loans to the banks and the banks are issuing new loans. The money supply falls dramatically when the banks slow the issuing of new loans. The banks do the exact opposite of what is needed to maintain a steady and healthy economy. They lend more when they need to slow down and they cut back when they need to lend more. They lend more when the economy is booming and lend less when the economy is contracting. This can be seen on the Greece graph above.

Two Money Systems.

Here we look at the two systems of money. They have the same unit but they are entirely different forms of money. They are linked together and work parallel to each other, but they are entirely different forms of money. The first is the Cash Currency that is the created by the central bank as folding paper notes (and a few coins). The second is Bank Credit as listed in bank accounts. Your bank balance is the amount of money the bank owes you, payable in real money which is Cash Currency. The system of moving Bank Credit from person to person enables a very efficient payment system. The problem lies with the debt that is constantly magnifying. In simple terms, to generate an extra million of Bank Credit as part of the money supply, a million of debt is created. To increase the money supply it is necessary to hang debts on more and more items that can have debts hung on them. If more debt is not created, the money supply cannot increase.

The Legal Definition of Money

I have problems trying to find a legal definition of money. It appears that the legal definition might as expressed by Professor Knapp:

Anything which is defined by the state as money is money. [Knapp 1924:158]

Professor Knapp, a Professor at Strasbourg University defines money as a system of tokens the state is willing to accept a payment of taxes. The state's unique role as a creditor, specifically the tax collector, authorizes it power to define money. [10075]

English economist, John Maynard Keynes, described it in these words:

anything which the State undertakes to accept at its pay-offices, whether or not it is declared legal-tender between citizens [10076]

The important characteristic of money is the ability that it gives to the holder to extinguish debt. One might prefer to define money as that which has been declared 'Legal Tender'. However, citizens may decide to use whatever they like as money and thus we would get some thinglike a definition used by The Supreme Court of Canada:

Any medium which by practice fulfills the function of money and which everyone will accept as payment of a debt is money in the ordinary sense of the word even though it may not be legal tender. , [10077]

The arguments are quite long and tedious. I gave you these snippets to warm you up so that you might decide for yourself whether Bank Credit should be classified as money. It perhaps depends on whether you believe that the government decides what is money or what citizens generally accept as being money. Bank Credit did not come from the government but was created at the time a loan was made and is thus credit. Although it can be used to extinguish debt and enables transactions, it is stretching things to claim that it is money. It is credit for money and, as such, has many of the characteristics of money.

Effect of a Fall in Money Supply

When the Money Supply falls under a Bank Credit regime, loan repayments are received by banks but fewer loans are granted. The loan repayments tend to come from the Circulating Money, rather than the Hoarded Money. Hoarded Money is held by 'those with more money than they can spend' and those with an inadequate supply of money are the borrowers. Thus, the Circulating Money section will decrease. A fall in velocity will be noticed. Those that consider the economy to be related to the gross Money Supply are incorrect as it is related to the Circulating Money portion of the Money Supply. My calculation for this makes an assumption of a cut off time of one month. One month being the difference between Circulating Money waiting for the next transaction and Hoarded Money that is held as a supposed store of value. This time may be overly generous, but it allows a calculation. So the Circulating Money percentage = (Velocity x Cut-off-time-in-weeks / 52) x 100%

| Velocity | Circulating Money | Hoarded Money |

| 12 | 100% | 0% |

| 10 | 83% | 17% |

| 5 | 42% | 58% |

| 3 | 25% | 75% |

| 2 | 17% | 83% |

| 1.5 | 12% | 88% |

| 1 | 8% | 92% |

| 0.75 | 6% | 94% |

| 0.5 | 4% | 96% |

So if the velocity is 2 (17% Circulating Money and 83% Hoarded Money) and the Money Supply falls 8%, the velocity has a tendency to fall to 1. The reason is that the 8% is largely taken from the 17% Circulating Money. It is not taken evenly between Circulating Money and Hoarded Money. So when there is a fall in the Money Supply, the Circulating Money takes a sharp fall destroying business as it does so.

When the Money Supply falls the bulk of the reduction occurs where it hurts most, in the Circulating Money component of the Money Supply. This magnifies the effect of the decrease. You can see this in the Great Depression Graph. 1928 Velocity = 1.5 and 1932 Velocity = 1.17 and by 1937 the money supply had recovered to its pre-Depression value but the velocity did not recover until 1943 and then had another fall. It also does not follow that an increase in the money supply will lift the economy as the increased money may find its way to 'those with more money than they can spend' and thus, it gets hoarded. If you want to recover an economy, it is better to go round villages and towns and give out small denomination notes to poor people the street who will spend it the same day. Or send out a bonus with welfare cheques.

A drop in the money supply tends to damage the economy because it reduces the Circulating Money to a greater degree than the fall in the money supply. (Reason: most of the reduction in Money Supply is taken from Circulating Money.) It is not reasonable to assume the reverse. If the money supply is increased, it may or may not boost the Circulating Money or it may become hoarded. This depends on whether it is spent to those with more than they can spend or to those with no savings. Even if the money is spent into the circulating component, businesses may have little ability to expand. Not every business will expand to match the market and many will have a delay in so doing. Expanding the economy is not as simple as increasing the money supply. Parameters need to be set to encourage businesses to expand. They should not have been treated so atrociously in the first place.

The Problem with Kings.

The banks have a problem when they lend money to a king. When a bank lends to a king, what happens to the debts when the king dies? Does the debt transfer to the next monarch? Or does the new monarch shout: "Off with their heads", with the reasoning that usury is prohibited in the bible. Whatever the answer, it is still a fairly large disincentive for a bank to lend to a king. The creditor class of old needed a better system so that their credit could be repaid with interest so that they could lend to a government with confidence. The solution was to remove the monarch or reduce the monarch to a figurehead. This had the advantage that the king lost the sovereignty over the creation of money. To hang a debt on the government and thus the people and the nation, it was deemed appropriate to give the people a say in government in the form of a vote. The system is called democracy. The next task was to control the way people vote and then to create political parties and control the parties. Public Opinion is controlled through a media system. Political parties are controlled through direct funding and funding of compliant parliamentarians. The debts owed to the creditors are payable with the taxes of the people. Revolutions are a convenient way of removing an established monarch. International war is a good way to destroy or bring to heel a recalcitrant nation. Any political party, that does not tow the line, gets the economy destroyed by the withholding of credit causing a severe fall in the money supply which leads to a recession or depression with its consequent unemployment, foreclosures and business bankruptcies, which is then blamed on the government. Both political parties support the debt banking system and every war that is advertised on the television.

John Adams (1735-1826)

There are two ways to conquer and enslave a nation. One is by sword. The other is by debt.

The Value of Money.

Money is an essential requirement for civilized life. The primary characteristic of money is that this initially valueless piece of paper enables the commercial transactions between citizens and businesses. I list this as:

The Third Flaw of Economics

Money has no value to the creator. The creator of money can create money tokens in any volume at effectively no cost. Money has no intrinsic value.

The magic of money is its ability to lubricate transactions. When a $20 note goes from A to B to C to D to E to F to G to H to I to J to K, it has enabled $200 worth of commercial transactions. As individuals, we value money by what we gain in the next transaction, but the real value of money is its ability to create many transactions. I usually tell this as a story:

I walk into a small quiet town that doesn't see many visitors. I get a haircut with a $20 note. The hairdresser buys some fresh fruit at the store. The farmer brings some more fruit around to the store. The farmer gets his four-wheel-drive repaired. The mechanic goes down the café and spends the $20 note. The café owner pays the cook. The cook gets his hair cut. This $20 note manages ten transactions on this day. One $20 note created $200 worth of transactions in one day. This is equivalent to 3650 transactions in the year which is described as a Velocity = 3650. This is $73000 of transactions from one $20 note. Very few notes ever manage this number of transactions in a year. They typically manage around two transactions in a year.

The rapid movement of the note ceases as soon as it reaches someone with too much money. The affluent person puts the note in a pocket and leaves it there. The worst thing that can happen to money is to hoard it. The next worst thing is to tax money that is actually creating transactions. Sales Tax and Income Tax would have destroyed our special $20 note before it had completed one lap. We are taxing money that is creating wealth-producing-transactions and leaving hoarded and speculative money untaxed. This is entirely the wrong way around. Money only does its job when it is passing from person to person. Money ceases to function as money when it is hoarded or used to push up the purchase price of assets. I give you this little story to show that the power of money lies in its ability to create transactions and using it as a store of value is counter productive to its primary purpose. This is the primary imperfection of money. When money is used as 'a store of value' it is not lubricating transactions and has thus ceased to act as money. I have a very neat way of making the citizenry more affluent by charging a neat little tax. It is called a Demurrage tax. It is a very small tax that discourages hoarding and makes money move much faster which makes everyone more affluent by more than the tax. I always thought that was the cleverest tax. A tax that makes you better off. The Demurrage tax is a small monthly tax on money holdings which encourages people to spend rather than hoard so they pay less of the economy-damaging income and sales taxes and get much higher benefit from the greater flow of money. You will need Demurrage tax of some kind in your perfect solution. It will be an unpopular medicine that is needed to correct the misuse of money.

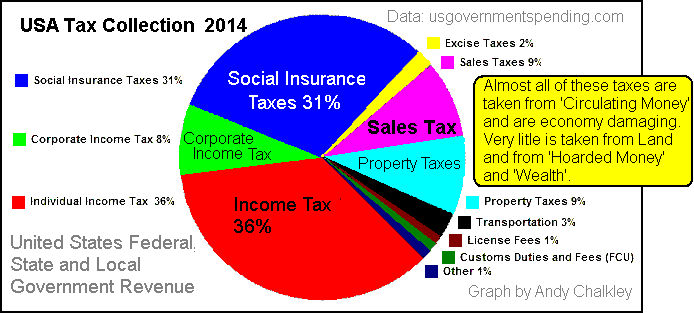

Tax

Our taxation system stifles trade. Under a sales tax regime, a percentage is removed at each transaction which heavily damps trade and real wealth creation. The same happens with income tax. It rapidly destroys trade and wealth creation. In the village example above, income tax and sales tax take a high percentage at each transaction between the egg trader, carrot grower, potato seller and customers, destroying the local economy. Hoarded Money is left entirely untouched and untaxed. The only tax that is collected is collected from well behaved Circulating Money that is dutifully carrying out its life's mission. Money that plays truant escapes taxation. It is not the money that suffers, but the whole of society by not allowing citizens the benefit of the potential transactions. If the velocity is increased, more transactions release their potential goods and services. How tax is collected not only influences economic activity, it also creates dangerous instability in ways that I shall explain. Yet there are tax regimes that don't discourage trade and economic activity. You will be unlikely to see them in your lifetime because of the scaremongering by those with enough money to modify Public Opinion, which happens to include your opinion. How much of your opinion has been modified by those with the ability to modify your opinion? The problem of taxing transactions is visible in this graph. This is not proof that increased transaction taxes decrease tax collection but it is enough to seriously challenge the talking heads that believe that an increase in income tax rate will result in greater tax collection. You should be able to find the points in this graph where decreased income tax rate, increased the tax collected.

Please do not move on until you have found the two points on the graph where tax rate reduction increased the tax collection. The reverse is not so clear.